Buy Now Pay Later Apps and Companies

Are Buy Now Pay Later Apps the future of payments? In an era marked by convenience and financial flexibility, these services have witnessed an unprecedented surge in popularity. This article delves into the compelling reasons behind the growing adoption of Buy Now Pay Later services, explores the key players in the industry, and provides valuable insights into how and where these services are reshaping the way we shop.What is Buy Now Pay Later Apps

Buy Now Pay Later (BNPL) apps are financial technology (FinTech) applications that provide consumers with the option to make purchases and delay the payment for those purchases until a later date. These apps offer an alternative to traditional credit cards and loans by allowing consumers to split their payments into smaller, often interest-free, installments.How BNPL apps typically work

Here’s how BNPL apps typically work: 1. Selection of Products or Services: Consumers browse online or visit a retail store to select products or services they want to purchase. 2. Checkout with BNPL: At the checkout stage, instead of paying the full purchase amount upfront, consumers can choose to pay using a BNPL app. 3. Payment Plan Options: BNPL apps offer various payment plan options, such as dividing the total cost into two, three, four, or more equal installments. Some apps may also offer longer-term financing options for larger purchases. 4. Approval and Affordability Check: The app may perform a quick approval process that assesses the consumer’s ability to make payments. This process is typically faster and less stringent than traditional credit checks. 5. Immediate Purchase: Once approved, consumers can complete the purchase and receive their chosen products or services immediately. 6. Payment Reminders: BNPL apps often send payment reminders to users before each installment is due to help them stay on track with their payments. 7. Repayment Flexibility: Many BNPL apps allow users to customize their repayment schedules or pay off the balance early without penalty, offering flexibility and control. 8. Mobile Accessibility: BNPL apps are typically accessible via mobile devices, making it convenient for users to manage their accounts, track payments, and access customer support.Why Is BNPL Gaining Popularity?

The rising popularity of BNPL services can be attributed to several compelling reasons: 1. Convenience BNPL services offer unparalleled convenience to consumers. They eliminate the need for credit checks and lengthy approval processes, allowing shoppers to complete transactions quickly and effortlessly. 2. Flexibility Consumers appreciate the flexibility BNPL services provide. They can choose from various repayment terms, often including interest-free options, allowing them to budget effectively and avoid high-interest credit card debt. 3. Transparency BNPL services are known for their transparent fee structures. Unlike credit cards with hidden charges, BNPL clearly outlines the repayment schedule, ensuring consumers are fully aware of their financial commitments. 4. Accessible to All BNPL services are inclusive, making them accessible to a wide range of consumers, including those with limited credit histories. This inclusivity appeals to younger demographics and those seeking alternative payment methods. 5. Enhanced Shopping Experience Retailers benefit from BNPL services too. They can attract more customers and increase conversion rates, leading to higher sales volumes.Key Statistic Data

Here are some key statistics related to the usage of Buy Now Pay Later (BNPL) services : 1. Global BNPL Market Growth The global BNPL market was valued at approximately $7.3 billion in 2020. It is projected to reach over $33.5 billion by 2027, with a CAGR of around 28% during the forecast period. (Source: Allied Market Research) 2. Consumer Adoption In the United States, nearly 45 million people had used a BNPL service by 2021. (Source: PYMNTS.com). 42% of U.S. consumers reported using BNPL services in 2020. (Source: The Ascent) 3. Age Demographics 50% of BNPL users in the U.S. are between the ages of 18 and 34. (Source: The Ascent). E-commerce Impact: BNPL usage has surged in e-commerce, with more than 70% of major U.S. online retailers offering BNPL options. (Source: The Motley Fool) 4. Basket Size Increase On average, consumers using BNPL tend to spend 55% more per transaction compared to traditional credit card users. (Source: Ascent Consumer Survey) 5. Reasons for Using BNPL 56% of BNPL users cite affordability and convenience as their primary reasons for using these services. (Source: The Motley Fool) 6. Default Rates BNPL default rates are relatively low, with some companies reporting default rates below 1%. (Source: Inside Higher Ed) 7. Global BNPL Leaders Some of the prominent BNPL companies include Afterpay, Klarna, Affirm, and PayPal’s Pay in 4. 8. Regulatory Scrutiny Governments and regulatory bodies have been considering increased oversight of BNPL services due to concerns about consumer debt and transparency. (Source: CNBC) 9. Merchant Benefits Merchants often report increased sales and conversion rates after implementing BNPL options. (Source: Business Insider)Where Are BNPL Services Making an Impact?

BNPL services have experienced exponential growth in various regions: 1. America In the United States, BNPL adoption has skyrocketed, with millions of consumers utilizing these services. Major retailers have integrated BNPL options into their online and in-store checkout processes. 2. Europe BNPL has gained significant traction in Europe, particularly in countries like the United Kingdom, Sweden, and Germany. European consumers are increasingly turning to BNPL for their shopping needs. 3. Australia Australia, where Afterpay was founded, has been a hotbed for BNPL adoption. The Australian market serves as a testament to the global appeal of these services. 4. Asia, Africa and Middle East The Asia and Middle East region has also witnessed a surge in BNPL usage. Companies like Klarna and Afterpay have expanded their presence in this burgeoning market.How Are BNPL Services Reshaping the Shopping Experience?

BNPL services are reshaping the shopping experience in profound ways: 1. Higher Average Order Values (AOVs) Shoppers using BNPL services tend to make larger purchases. The flexibility of installment payments encourages customers to buy more, increasing AOVs for retailers. 2. Reduced Cart Abandonment BNPL services can significantly reduce cart abandonment rates. When faced with a large purchase, consumers are more likely to proceed when offered the option to split the cost. 3. Increased Conversion Rates Retailers offering BNPL options report higher conversion rates. Shoppers who may have hesitated due to upfront costs are more likely to convert when they can defer payments.Who Are the Major Players in the BNPL Industry?

Several companies have emerged as dominant forces in the BNPL landscape. These companies provide the platforms and infrastructure that enable consumers to experience the benefits of BNPL services. 27 Buy Now Pay Later Apps and companies include (Updated October 3rd 2023):1. Afterpay

Afterpay is a prominent Buy Now Pay Later (BNPL) app that has gained widespread popularity for its convenience in online and in-store shopping. It allows users to make purchases and split the payment into four equal installments, payable over a six-week period. Afterpay partners with a wide range of retailers, offering a flexible and interest-free payment option for consumers. Afterpay is available in multiple countries, including the United States, the United Kingdom, Australia, Canada, and more. Features: 1. Four Equal Payments: Afterpay divides the total purchase amount into four equal payments, with the first installment paid at the time of purchase. 2. No Interest (on Most Plans): In most cases, Afterpay does not charge interest, making it an attractive option for budget-conscious shoppers. 3. Instant Approval: The approval process is quick, allowing users to complete their transactions without delay. 4. Mobile Accessibility: Afterpay is available as a mobile app, making it easy for users to manage their payments and accounts on the go. 5. Retailer Partnerships: Afterpay partners with a vast network of retailers, both online and in physical stores, across various industries. Pros: 1. Payment Flexibility: Afterpay offers users the flexibility to budget for their purchases and manage their finances effectively. 2. Interest-Free Options: In most cases, Afterpay does not charge interest, which can save users money compared to credit cards. 3. No Credit Checks: Users do not undergo traditional credit checks when using Afterpay, making it accessible to a wide range of consumers. 4. Transparency: Afterpay provides clear information about payment schedules and any applicable fees. Cons: 1. Late Fees: Missing payments can result in late fees, potentially increasing the overall cost of the purchase. 2. Limited to Four Payments: Afterpay’s structure limits users to four payments, which may not suit larger or longer-term purchases. 3. Not Suitable for All Retailers: While Afterpay partners with many retailers, not all stores accept Afterpay as a payment option.

Features: 1. Four Equal Payments: Afterpay divides the total purchase amount into four equal payments, with the first installment paid at the time of purchase. 2. No Interest (on Most Plans): In most cases, Afterpay does not charge interest, making it an attractive option for budget-conscious shoppers. 3. Instant Approval: The approval process is quick, allowing users to complete their transactions without delay. 4. Mobile Accessibility: Afterpay is available as a mobile app, making it easy for users to manage their payments and accounts on the go. 5. Retailer Partnerships: Afterpay partners with a vast network of retailers, both online and in physical stores, across various industries. Pros: 1. Payment Flexibility: Afterpay offers users the flexibility to budget for their purchases and manage their finances effectively. 2. Interest-Free Options: In most cases, Afterpay does not charge interest, which can save users money compared to credit cards. 3. No Credit Checks: Users do not undergo traditional credit checks when using Afterpay, making it accessible to a wide range of consumers. 4. Transparency: Afterpay provides clear information about payment schedules and any applicable fees. Cons: 1. Late Fees: Missing payments can result in late fees, potentially increasing the overall cost of the purchase. 2. Limited to Four Payments: Afterpay’s structure limits users to four payments, which may not suit larger or longer-term purchases. 3. Not Suitable for All Retailers: While Afterpay partners with many retailers, not all stores accept Afterpay as a payment option.2. Klarna

Klarna is a leading Buy Now Pay Later (BNPL) service provider that operates globally, offering users the ability to shop online and pay for their purchases later. Founded in Sweden, Klarna has become known for its smooth and convenient payment solutions. It partners with a vast network of retailers, making it accessible to shoppers in various countries. Klarna has a strong global presence, serving consumers and retailers in numerous countries across Europe, the United States, and beyond. It offers localized services to cater to the needs of customers in different regions. Features: 1. Pay Later Option: Klarna allows users to make purchases and defer payment for a set period, typically up to 30 days, without incurring interest charges. 2. Installment Plans: Klarna also offers installment payment plans, allowing users to split the cost of their purchases into several equal payments over a longer period. These may have associated interest charges depending on the terms. 3. Smooth Checkout Integration: Klarna’s payment solution integrates seamlessly into the checkout process of partnering retailers, making it easy for users to select Klarna as a payment option. 4. Mobile App: Klarna provides a mobile app for users to manage their purchases, track payments, and explore new shopping opportunities. Pros: 1. Flexible Payment Options: Klarna offers both short-term deferred payments and installment plans, catering to a variety of consumer preferences. 2. Global Reach: Klarna’s wide geographic coverage ensures that users from various countries can access and benefit from its services. 3. User-Friendly: Klarna’s interface is user-friendly and integrates seamlessly with many online retailers, simplifying the shopping and payment process. 4. Protection for Buyers: Klarna offers a Buyer’s Protection policy that safeguards users in case of order issues or disputes. Cons: 1. Interest Charges: While Klarna offers interest-free options for short-term payments, users opting for longer-term installment plans may incur interest charges, which should be carefully considered. 2. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of purchases. 3. Not Universal: Klarna may not be accepted by all retailers, limiting its availability in certain online stores.

Features: 1. Pay Later Option: Klarna allows users to make purchases and defer payment for a set period, typically up to 30 days, without incurring interest charges. 2. Installment Plans: Klarna also offers installment payment plans, allowing users to split the cost of their purchases into several equal payments over a longer period. These may have associated interest charges depending on the terms. 3. Smooth Checkout Integration: Klarna’s payment solution integrates seamlessly into the checkout process of partnering retailers, making it easy for users to select Klarna as a payment option. 4. Mobile App: Klarna provides a mobile app for users to manage their purchases, track payments, and explore new shopping opportunities. Pros: 1. Flexible Payment Options: Klarna offers both short-term deferred payments and installment plans, catering to a variety of consumer preferences. 2. Global Reach: Klarna’s wide geographic coverage ensures that users from various countries can access and benefit from its services. 3. User-Friendly: Klarna’s interface is user-friendly and integrates seamlessly with many online retailers, simplifying the shopping and payment process. 4. Protection for Buyers: Klarna offers a Buyer’s Protection policy that safeguards users in case of order issues or disputes. Cons: 1. Interest Charges: While Klarna offers interest-free options for short-term payments, users opting for longer-term installment plans may incur interest charges, which should be carefully considered. 2. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of purchases. 3. Not Universal: Klarna may not be accepted by all retailers, limiting its availability in certain online stores.3. Affirm

Affirm is a prominent Buy Now Pay Later (BNPL) service provider based in the United States, offering consumers an alternative payment method for online and in-store purchases. Founded by Max Levchin, one of the co-founders of PayPal, Affirm focuses on providing flexible financing options that allow users to make purchases and repay over time with clear terms and transparency. While Affirm is headquartered in the United States, it serves consumers and partners with various retailers across the country. Affirm operates within the United States, U.S. territories and Canada. Features: 1. Point-of-Sale Financing: Affirm offers point-of-sale financing, allowing users to select Affirm as a payment option when making purchases online or in participating physical stores. 2. Transparent Terms: Affirm provides clear information about interest rates, repayment terms, and monthly payments, ensuring users have a comprehensive understanding of their financing. 3. Flexible Repayment Plans: Users can choose from various repayment plans, including short-term and longer-term options, depending on the specific terms offered by participating retailers. 4. Mobile Accessibility: Affirm offers a mobile app that allows users to manage their accounts, view payment schedules, and access customer support. Pros: 1. Payment Flexibility: Affirm provides flexible financing options, making it easier for users to budget for their purchases and manage their finances. 2. Clear Terms: Affirm’s transparency regarding interest rates and repayment terms helps users make informed financial decisions. 3. No Hidden Fees: The service aims to be transparent about its fees and interest rates, reducing the risk of unexpected charges. 4. Improved Shopping Experience: Affirm’s financing options can enhance the shopping experience, encouraging users to complete purchases they might have otherwise postponed. Cons: 1. Interest Charges: Depending on the terms selected and the retailer, users may incur interest charges when choosing Affirm for financing. Reviewing these terms is crucial. 2. Late Fees: Missing payments or making late payments can result in late fees, which can increase the overall cost of the purchase. 3. Limited Geographic Coverage: As of my last knowledge update, Affirm primarily served customers within the United States. Users outside of this region may not have access to its services.

Features: 1. Point-of-Sale Financing: Affirm offers point-of-sale financing, allowing users to select Affirm as a payment option when making purchases online or in participating physical stores. 2. Transparent Terms: Affirm provides clear information about interest rates, repayment terms, and monthly payments, ensuring users have a comprehensive understanding of their financing. 3. Flexible Repayment Plans: Users can choose from various repayment plans, including short-term and longer-term options, depending on the specific terms offered by participating retailers. 4. Mobile Accessibility: Affirm offers a mobile app that allows users to manage their accounts, view payment schedules, and access customer support. Pros: 1. Payment Flexibility: Affirm provides flexible financing options, making it easier for users to budget for their purchases and manage their finances. 2. Clear Terms: Affirm’s transparency regarding interest rates and repayment terms helps users make informed financial decisions. 3. No Hidden Fees: The service aims to be transparent about its fees and interest rates, reducing the risk of unexpected charges. 4. Improved Shopping Experience: Affirm’s financing options can enhance the shopping experience, encouraging users to complete purchases they might have otherwise postponed. Cons: 1. Interest Charges: Depending on the terms selected and the retailer, users may incur interest charges when choosing Affirm for financing. Reviewing these terms is crucial. 2. Late Fees: Missing payments or making late payments can result in late fees, which can increase the overall cost of the purchase. 3. Limited Geographic Coverage: As of my last knowledge update, Affirm primarily served customers within the United States. Users outside of this region may not have access to its services.4. Sezzle

Sezzle is a Buy Now Pay Later (BNPL) apps that offers consumers a flexible and interest-free payment option for online and in-store purchases. With a focus on transparency and affordability, Sezzle aims to provide users with the ability to split their payments into manageable installments over time. Sezzle primarily served customers in the United States and Canada. Features: 1. Interest-Free Payments: Sezzle typically offers interest-free installment plans, allowing users to spread their purchase cost over several payments without accruing interest charges. 2. Quick Approval: Sezzle’s approval process is quick, enabling users to receive approval and complete their transactions swiftly. 3. Transparent Terms: Sezzle provides clear information about repayment terms and schedules, helping users make informed financial decisions. 4. Online and In-Store Use: Users can use Sezzle for both online and in-store purchases, making it versatile for various shopping experiences. 5. Customizable Payment Plans: Sezzle allows users to customize their payment plans, including the number of installments and payment frequency. Pros: 1. Affordability: Sezzle’s interest-free payment plans make it an affordable option for budget-conscious shoppers. 2. No Credit Checks: Sezzle typically does not perform traditional credit checks, making it accessible to users with varying credit histories. 3. Convenience: The service enhances the shopping experience by offering a convenient and flexible payment method. 4. Mobile Accessibility: Sezzle provides a mobile app for users to manage their accounts and payments on the go. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, which can increase the overall cost of purchases. 2. Limited Geographic Coverage: Sezzle’s availability may be limited to certain regions, so users outside of supported areas may not have access to the service. 3. Varying Retailer Acceptance: Not all retailers accept Sezzle, so users should check whether their preferred stores offer Sezzle as a payment option.

Features: 1. Interest-Free Payments: Sezzle typically offers interest-free installment plans, allowing users to spread their purchase cost over several payments without accruing interest charges. 2. Quick Approval: Sezzle’s approval process is quick, enabling users to receive approval and complete their transactions swiftly. 3. Transparent Terms: Sezzle provides clear information about repayment terms and schedules, helping users make informed financial decisions. 4. Online and In-Store Use: Users can use Sezzle for both online and in-store purchases, making it versatile for various shopping experiences. 5. Customizable Payment Plans: Sezzle allows users to customize their payment plans, including the number of installments and payment frequency. Pros: 1. Affordability: Sezzle’s interest-free payment plans make it an affordable option for budget-conscious shoppers. 2. No Credit Checks: Sezzle typically does not perform traditional credit checks, making it accessible to users with varying credit histories. 3. Convenience: The service enhances the shopping experience by offering a convenient and flexible payment method. 4. Mobile Accessibility: Sezzle provides a mobile app for users to manage their accounts and payments on the go. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, which can increase the overall cost of purchases. 2. Limited Geographic Coverage: Sezzle’s availability may be limited to certain regions, so users outside of supported areas may not have access to the service. 3. Varying Retailer Acceptance: Not all retailers accept Sezzle, so users should check whether their preferred stores offer Sezzle as a payment option.5. PayPal Pay in 4

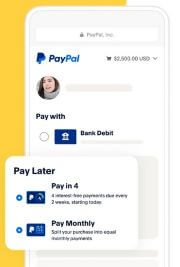

PayPal Pay in 4 is a Buy Now Pay Later (BNPL) service offered by PayPal, a well-known and globally recognized payment platform. This BNPL option allows users to split their purchases into four equal payments over a six-week period, making it easier for shoppers to budget and manage their expenses. PayPal Pay in 4 is available in the United States and certain other countries where PayPal services are offered. Features: 1. Four Equal Payments: PayPal Pay in 4 divides the total purchase amount into four equal installments, with the first payment due at the time of purchase. 2. No Interest (on Most Plans): In most cases, PayPal Pay in 4 does not charge interest, providing users with an interest-free financing option. 3. Quick Approval: Users can receive quick approval for PayPal Pay in 4, facilitating smooth and timely transactions. 4. Online and In-Store Use: PayPal Pay in 4 can be used for both online and in-store purchases, offering versatility in shopping experiences. 5. PayPal Integration: This BNPL service is seamlessly integrated with users’ existing PayPal accounts, streamlining the payment process. Pros: 1. Flexible Payments: PayPal Pay in 4 offers flexibility by allowing users to spread their payments over a brief period, making it easier to manage expenses. 2. No Interest (on Most Plans): Users can enjoy interest-free financing for most transactions, potentially saving money compared to traditional credit cards. 3. Quick Checkout: Integration with PayPal accounts ensures a quick and hassle-free checkout process. 4. Mobile Accessibility: PayPal provides a mobile app that allows users to manage their payments and accounts conveniently on their smartphones. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of purchases. 2. Limited Geographic Coverage: PayPal Pay in 4 may not be available in all regions. 3. Credit Impact: While PayPal Pay in 4 doesn’t perform traditional credit checks, missed payments may negatively affect users’ PayPal accounts.

Features: 1. Four Equal Payments: PayPal Pay in 4 divides the total purchase amount into four equal installments, with the first payment due at the time of purchase. 2. No Interest (on Most Plans): In most cases, PayPal Pay in 4 does not charge interest, providing users with an interest-free financing option. 3. Quick Approval: Users can receive quick approval for PayPal Pay in 4, facilitating smooth and timely transactions. 4. Online and In-Store Use: PayPal Pay in 4 can be used for both online and in-store purchases, offering versatility in shopping experiences. 5. PayPal Integration: This BNPL service is seamlessly integrated with users’ existing PayPal accounts, streamlining the payment process. Pros: 1. Flexible Payments: PayPal Pay in 4 offers flexibility by allowing users to spread their payments over a brief period, making it easier to manage expenses. 2. No Interest (on Most Plans): Users can enjoy interest-free financing for most transactions, potentially saving money compared to traditional credit cards. 3. Quick Checkout: Integration with PayPal accounts ensures a quick and hassle-free checkout process. 4. Mobile Accessibility: PayPal provides a mobile app that allows users to manage their payments and accounts conveniently on their smartphones. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of purchases. 2. Limited Geographic Coverage: PayPal Pay in 4 may not be available in all regions. 3. Credit Impact: While PayPal Pay in 4 doesn’t perform traditional credit checks, missed payments may negatively affect users’ PayPal accounts.6. Splitit

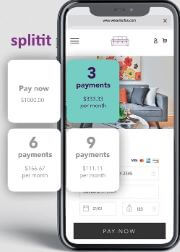

Splitit is a Buy Now Pay Later (BNPL) service that offers consumers a unique payment solution for making purchases. Unlike traditional BNPL services, Splitit allows users to split the cost of their purchases into interest-free monthly installments using their existing credit cards. This service focuses on providing budget-friendly and flexible payment options. Splitit had a global presence, serving consumers and partnering with retailers in various countries such as United States, United Kingdom, Australia and Japan. The service aimed to be available to users and retailers worldwide. Features: 1. Use of Existing Credit Cards: Splitit allows users to make purchases using their existing credit cards, with no need to apply for new credit or undergo additional credit checks. 2. Interest-Free Payments: Splitit typically offers interest-free installment plans, with users not incurring interest charges on their purchases. 3. Flexible Payment Plans: Users can customize their payment plans, choosing the number of installments that best fit their budget and preferences. 4. Online and In-Store Use: Splitit can be used for both online and in-store purchases, offering versatility in shopping experiences. 5. Transparent Fees: Splitit aims to be transparent about its fees, providing users with clear information about their installment plans. Pros: 1. Use of Existing Credit Cards: Users can take advantage of Splitit’s services without the need for new credit applications or additional financial checks. 2. Interest-Free Payments: Most Splitit plans are interest-free, allowing users to make purchases without accruing interest charges. 3. Payment Flexibility: Users can tailor their payment plans to match their financial situation, making budgeting more manageable. 4. Versatility: Splitit can be used for various types of purchases, both online and in physical stores. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of purchases. 2. Limited Acceptance: While Splitit partners with numerous retailers, not all stores may accept Splitit as a payment option. 3. Credit Card Utilization: Splitit may impact the available credit on users’ credit cards while installment payments are active.

Features: 1. Use of Existing Credit Cards: Splitit allows users to make purchases using their existing credit cards, with no need to apply for new credit or undergo additional credit checks. 2. Interest-Free Payments: Splitit typically offers interest-free installment plans, with users not incurring interest charges on their purchases. 3. Flexible Payment Plans: Users can customize their payment plans, choosing the number of installments that best fit their budget and preferences. 4. Online and In-Store Use: Splitit can be used for both online and in-store purchases, offering versatility in shopping experiences. 5. Transparent Fees: Splitit aims to be transparent about its fees, providing users with clear information about their installment plans. Pros: 1. Use of Existing Credit Cards: Users can take advantage of Splitit’s services without the need for new credit applications or additional financial checks. 2. Interest-Free Payments: Most Splitit plans are interest-free, allowing users to make purchases without accruing interest charges. 3. Payment Flexibility: Users can tailor their payment plans to match their financial situation, making budgeting more manageable. 4. Versatility: Splitit can be used for various types of purchases, both online and in physical stores. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of purchases. 2. Limited Acceptance: While Splitit partners with numerous retailers, not all stores may accept Splitit as a payment option. 3. Credit Card Utilization: Splitit may impact the available credit on users’ credit cards while installment payments are active.7. Zip

Zip is a Buy Now Pay Later (BNPL) service that offers consumers flexible payment options for their online and in-store purchases. Originally established in Australia, Zip has expanded its services to various countries, providing users with the ability to split their payments into interest-free installments or choose longer-term financing options. Zip has a growing global presence and serves consumers and retailers in several countries such as United States, United Kingdom, Canada, Australia and New Zealand. Features: 1. Interest-Free Payments: Zip typically offers interest-free installment plans, enabling users to divide their purchase cost into equal payments without incurring additional interest charges. 2. Longer-Term Financing: In addition to installment plans, Zip may offer longer-term financing options for larger purchases, subject to specific terms. 3. Quick Approval: Users can undergo a quick approval process, allowing for a streamlined shopping experience. 4. Online and In-Store Use: Zip can be used for both online and in-store purchases, providing versatility for different shopping scenarios. 5. Mobile Accessibility: Zip offers a mobile app that allows users to manage their accounts, view payment schedules, and access customer support conveniently. Pros: 1. Interest-Free Payments: Most Zip installment plans are interest-free, providing users with a budget-friendly payment solution. 2. Payment Flexibility: Zip offers both short-term and longer-term financing options, catering to various consumer preferences and budgets. 3. Quick Checkout: The integration with participating retailers ensures a seamless and efficient checkout process. 4. Mobile App: The Zip mobile app allows users to manage their payments and accounts on their smartphones, enhancing accessibility. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of purchases. 2. Limited Acceptance: While Zip partners with many retailers, not all stores may accept Zip as a payment option. 3. Credit Impact: While Zip may not conduct traditional credit checks, missed payments may negatively affect users’ creditworthiness.

Features: 1. Interest-Free Payments: Zip typically offers interest-free installment plans, enabling users to divide their purchase cost into equal payments without incurring additional interest charges. 2. Longer-Term Financing: In addition to installment plans, Zip may offer longer-term financing options for larger purchases, subject to specific terms. 3. Quick Approval: Users can undergo a quick approval process, allowing for a streamlined shopping experience. 4. Online and In-Store Use: Zip can be used for both online and in-store purchases, providing versatility for different shopping scenarios. 5. Mobile Accessibility: Zip offers a mobile app that allows users to manage their accounts, view payment schedules, and access customer support conveniently. Pros: 1. Interest-Free Payments: Most Zip installment plans are interest-free, providing users with a budget-friendly payment solution. 2. Payment Flexibility: Zip offers both short-term and longer-term financing options, catering to various consumer preferences and budgets. 3. Quick Checkout: The integration with participating retailers ensures a seamless and efficient checkout process. 4. Mobile App: The Zip mobile app allows users to manage their payments and accounts on their smartphones, enhancing accessibility. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of purchases. 2. Limited Acceptance: While Zip partners with many retailers, not all stores may accept Zip as a payment option. 3. Credit Impact: While Zip may not conduct traditional credit checks, missed payments may negatively affect users’ creditworthiness.8. Laybuy

Laybuy is a Buy Now Pay Later (BNPL) service that offers consumers a flexible payment solution for their online and in-store purchases. Hailing from New Zealand, Laybuy has expanded its services to various countries, allowing users to divide their payments into interest-free installments and manage their finances effectively. Laybuy has expanded its services to several countries, including the United Kingdom, Australia, and others. While the service continues to grow, it’s advisable to verify if Laybuy’s offerings are available in your specific region. Features: 1. Interest-Free Payments: Laybuy typically offers interest-free installment plans, allowing users to split their purchase cost into equal payments without incurring additional interest charges. 2. Quick Approval: Laybuy provides a swift approval process, ensuring a seamless shopping experience. 3. Flexible Payment Plans: Users can choose the number of installments that best suit their budget and financial preferences. 4. Online and In-Store Use: Laybuy can be used for both online and in-store purchases, providing flexibility for various shopping scenarios. 5. Mobile Accessibility: Laybuy offers a mobile app that allows users to manage their accounts, track payments, and access customer support conveniently. Pros: 1. Interest-Free Payments: Most Laybuy installment plans are interest-free, offering users an affordable and budget-friendly payment option. 2. Payment Flexibility: Laybuy provides users with the flexibility to customize their payment plans, catering to various budgets. 3. Quick Checkout: Integration with participating retailers ensures a smooth and efficient checkout process. 4. Mobile App: Laybuy’s mobile app enhances accessibility, allowing users to manage their accounts and payments on the go. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of purchases. 2. Limited Retailer Acceptance: While Laybuy partners with numerous retailers, not all stores may accept Laybuy as a payment option. 3. Credit Impact: While Laybuy may not conduct traditional credit checks, missed payments may negatively affect users’ credit profiles.

Features: 1. Interest-Free Payments: Laybuy typically offers interest-free installment plans, allowing users to split their purchase cost into equal payments without incurring additional interest charges. 2. Quick Approval: Laybuy provides a swift approval process, ensuring a seamless shopping experience. 3. Flexible Payment Plans: Users can choose the number of installments that best suit their budget and financial preferences. 4. Online and In-Store Use: Laybuy can be used for both online and in-store purchases, providing flexibility for various shopping scenarios. 5. Mobile Accessibility: Laybuy offers a mobile app that allows users to manage their accounts, track payments, and access customer support conveniently. Pros: 1. Interest-Free Payments: Most Laybuy installment plans are interest-free, offering users an affordable and budget-friendly payment option. 2. Payment Flexibility: Laybuy provides users with the flexibility to customize their payment plans, catering to various budgets. 3. Quick Checkout: Integration with participating retailers ensures a smooth and efficient checkout process. 4. Mobile App: Laybuy’s mobile app enhances accessibility, allowing users to manage their accounts and payments on the go. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of purchases. 2. Limited Retailer Acceptance: While Laybuy partners with numerous retailers, not all stores may accept Laybuy as a payment option. 3. Credit Impact: While Laybuy may not conduct traditional credit checks, missed payments may negatively affect users’ credit profiles.9. Humm (formerly Certegy Ezi-Pay)

Humm is a Buy Now Pay Later (BNPL) service that provides consumers with flexible payment options for their online and in-store purchases. Originally established in Australia and New Zealand, Humm has expanded its services to other countries, offering users the ability to split their payments into manageable installments and improve their financial flexibility. Humm has extended its services to several countries, including Australia, New Zealand, Ireland, and others. Features: 1. Interest-Free Payments: Humm typically offers interest-free installment plans, allowing users to divide their purchase cost into equal payments without incurring additional interest charges. 2. Quick Approval: Humm provides a swift approval process, ensuring a seamless shopping experience. 3. Flexible Payment Plans: Users can customize their payment plans, selecting the number of installments that align with their budget and financial preferences. 4. Online and In-Store Use: Humm can be used for both online and in-store purchases, providing versatility for various shopping scenarios. 5. Mobile Accessibility: Humm offers a mobile app that allows users to manage their accounts, track payments, and access customer support conveniently. Pros: 1. Interest-Free Payments: Most Humm installment plans are interest-free, providing users with an affordable and budget-friendly payment option. 2. Payment Flexibility: Humm offers users the flexibility to tailor their payment plans to match their financial situation. 3. Quick Checkout: Integration with participating retailers ensures a smooth and efficient checkout process. 4. Mobile App: Humm’s mobile app enhances accessibility, allowing users to manage their accounts and payments on the go. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of purchases. 2. Limited Retailer Acceptance: While Humm partners with numerous retailers, not all stores may accept Humm as a payment option. 3. Credit Impact: While Humm may not conduct traditional credit checks, missed payments may negatively affect users’ credit profiles.

Features: 1. Interest-Free Payments: Humm typically offers interest-free installment plans, allowing users to divide their purchase cost into equal payments without incurring additional interest charges. 2. Quick Approval: Humm provides a swift approval process, ensuring a seamless shopping experience. 3. Flexible Payment Plans: Users can customize their payment plans, selecting the number of installments that align with their budget and financial preferences. 4. Online and In-Store Use: Humm can be used for both online and in-store purchases, providing versatility for various shopping scenarios. 5. Mobile Accessibility: Humm offers a mobile app that allows users to manage their accounts, track payments, and access customer support conveniently. Pros: 1. Interest-Free Payments: Most Humm installment plans are interest-free, providing users with an affordable and budget-friendly payment option. 2. Payment Flexibility: Humm offers users the flexibility to tailor their payment plans to match their financial situation. 3. Quick Checkout: Integration with participating retailers ensures a smooth and efficient checkout process. 4. Mobile App: Humm’s mobile app enhances accessibility, allowing users to manage their accounts and payments on the go. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of purchases. 2. Limited Retailer Acceptance: While Humm partners with numerous retailers, not all stores may accept Humm as a payment option. 3. Credit Impact: While Humm may not conduct traditional credit checks, missed payments may negatively affect users’ credit profiles.10. SplitPay

SplitPay is a Buy Now, Pay Later (BNPL) provider that allows customers to split their purchases into equal installments, typically three or four, with no interest or fees. It is currently available in the United Kingdom, Australia, and New Zealand. Features: 1. Split purchases into equal installments, typically three or four, with no interest or fees. 2. Shop at participating retailers online and in-store. 3. Quick and easy application process. 4. No credit check required. 5. Flexible repayment options. Pros: 1. Convenient way to spread out the cost of purchases. 2. Can help consumers budget their money more effectively. 3. May help consumers avoid high-interest debt. 4. Can help consumers build their credit history. Cons: 1. Late payments may result in fees and interest charges. 2. May encourage overspending. 3. Can lead to debt problems if not managed carefully.

Features: 1. Split purchases into equal installments, typically three or four, with no interest or fees. 2. Shop at participating retailers online and in-store. 3. Quick and easy application process. 4. No credit check required. 5. Flexible repayment options. Pros: 1. Convenient way to spread out the cost of purchases. 2. Can help consumers budget their money more effectively. 3. May help consumers avoid high-interest debt. 4. Can help consumers build their credit history. Cons: 1. Late payments may result in fees and interest charges. 2. May encourage overspending. 3. Can lead to debt problems if not managed carefully.11. Uplift

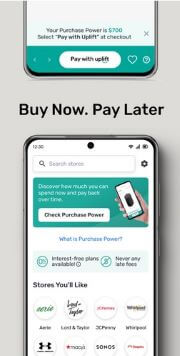

Uplift is a Buy Now Pay Later (BNPL) app that offers consumers a flexible and convenient way to finance their travel and vacation expenses. This app is specifically designed to make travel more accessible by allowing users to spread the cost of their trips over a set period. Uplift partners with various travel companies and platforms, enabling travelers to plan and book their dream vacations with ease. It is currently available in the United States and Canada. Features: 1. Travel Financing: Uplift specializes in travel-related expenses, including flights, accommodations, cruises, and vacation packages. 2. Flexible Payment Plans: Users can choose from various payment plans, often with competitive interest rates and terms that suit their budget. 3. Transparent Fees: Uplift provides clear information about fees and interest rates, ensuring users understand the cost of financing their travel. 4. Instant Approval: The app offers quick approval processes, allowing travelers to finalize their bookings without delays. 5. Early Repayment: Users have the flexibility to pay off their travel loans ahead of schedule without penalties. 6. Travel Partnerships: Uplift partners with a wide range of travel companies, making it accessible to travelers booking through participating providers. Pros: 1. Accessible Travel: Uplift helps users make their travel dreams a reality by offering financing options for expensive trips. 2. Payment Flexibility: The app provides various payment plans, making it easier for travelers to budget for their vacations. 3. No Hidden Fees: Uplift is transparent about its fees, helping users make informed decisions. 4. Quick Approval: Users can receive approval quickly, making it convenient for last-minute travel bookings. Cons: 1. Limited Use: Uplift is primarily designed for travel financing and may not be suitable for general retail purchases. 2. Interest Charges: While some payment plans may be interest-free, others may have interest charges, so users should carefully review terms. 3. Late Fees: Missing payments can result in late fees, potentially increasing the overall cost of the trip.

Features: 1. Travel Financing: Uplift specializes in travel-related expenses, including flights, accommodations, cruises, and vacation packages. 2. Flexible Payment Plans: Users can choose from various payment plans, often with competitive interest rates and terms that suit their budget. 3. Transparent Fees: Uplift provides clear information about fees and interest rates, ensuring users understand the cost of financing their travel. 4. Instant Approval: The app offers quick approval processes, allowing travelers to finalize their bookings without delays. 5. Early Repayment: Users have the flexibility to pay off their travel loans ahead of schedule without penalties. 6. Travel Partnerships: Uplift partners with a wide range of travel companies, making it accessible to travelers booking through participating providers. Pros: 1. Accessible Travel: Uplift helps users make their travel dreams a reality by offering financing options for expensive trips. 2. Payment Flexibility: The app provides various payment plans, making it easier for travelers to budget for their vacations. 3. No Hidden Fees: Uplift is transparent about its fees, helping users make informed decisions. 4. Quick Approval: Users can receive approval quickly, making it convenient for last-minute travel bookings. Cons: 1. Limited Use: Uplift is primarily designed for travel financing and may not be suitable for general retail purchases. 2. Interest Charges: While some payment plans may be interest-free, others may have interest charges, so users should carefully review terms. 3. Late Fees: Missing payments can result in late fees, potentially increasing the overall cost of the trip.12. Fly Now Pay Later

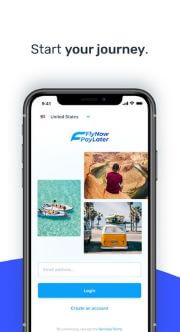

Fly Now Pay Later is a specialized Buy Now Pay Later (BNPL) service that focuses on providing financing options for travelers. This BNPL service aims to make travel more accessible by allowing users to book flights, accommodations, and other travel-related expenses and pay for them in manageable installments. Fly Now Pay Later primarily serves customers in the United Kingdom, where it has established partnerships with various travel companies and airlines. Features: 1. Travel Financing: Fly Now Pay Later specializes in travel-related expenses, including flights, hotels, vacation packages, and more. 2. Interest-Free Options: Users can typically choose interest-free installment plans for their travel bookings, making it easier to budget for trips. 3. Quick Approval: Fly Now Pay Later offers a swift approval process, allowing users to finalize their travel plans without delays. 4. Flexible Payment Plans: Users can customize their payment plans, selecting the number of installments and the repayment frequency that suits their budget. 5. Booking Flexibility: Fly Now Pay Later is integrated with various travel booking platforms, making it convenient for users to plan and book their trips. Pros: 1. Accessible Travel: Fly Now Pay Later helps users finance their dream vacations, making travel more accessible and budget-friendly. 2. Interest-Free Payments: Most Fly Now Pay Later plans are interest-free, allowing users to avoid interest charges on their travel expenses. 3. Quick Checkout: Integration with travel booking platforms ensures a seamless and efficient booking process. 4. Mobile Accessibility: Fly Now Pay Later may offer a mobile app, providing users with easy access to their travel bookings and payment information. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of the trip. 2. Limited Geographic Coverage: Fly Now Pay Later’s primary focus may be on the United Kingdom, limiting availability in other regions. 3. Credit Impact: While Fly Now Pay Later may not conduct traditional credit checks, missed payments may negatively affect users’ credit profiles.

Features: 1. Travel Financing: Fly Now Pay Later specializes in travel-related expenses, including flights, hotels, vacation packages, and more. 2. Interest-Free Options: Users can typically choose interest-free installment plans for their travel bookings, making it easier to budget for trips. 3. Quick Approval: Fly Now Pay Later offers a swift approval process, allowing users to finalize their travel plans without delays. 4. Flexible Payment Plans: Users can customize their payment plans, selecting the number of installments and the repayment frequency that suits their budget. 5. Booking Flexibility: Fly Now Pay Later is integrated with various travel booking platforms, making it convenient for users to plan and book their trips. Pros: 1. Accessible Travel: Fly Now Pay Later helps users finance their dream vacations, making travel more accessible and budget-friendly. 2. Interest-Free Payments: Most Fly Now Pay Later plans are interest-free, allowing users to avoid interest charges on their travel expenses. 3. Quick Checkout: Integration with travel booking platforms ensures a seamless and efficient booking process. 4. Mobile Accessibility: Fly Now Pay Later may offer a mobile app, providing users with easy access to their travel bookings and payment information. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of the trip. 2. Limited Geographic Coverage: Fly Now Pay Later’s primary focus may be on the United Kingdom, limiting availability in other regions. 3. Credit Impact: While Fly Now Pay Later may not conduct traditional credit checks, missed payments may negatively affect users’ credit profiles.13. Ginny’s

Ginny’s is a Buy Now, Pay Later (BNPL) provider that allows customers to split their purchases into equal installments, typically four, with no interest or fees. It is currently available in the United States. Features: 1. Split purchases into equal installments, typically four, with no interest or fees. 2. Shop at participating retailers online and in-store. 3. Quick and easy application process. 4. No credit check required. 5. Flexible repayment options. Pros: 1. Convenient way to spread out the cost of purchases. 2. Can help consumers budget their money more effectively. 3. May help consumers avoid high-interest debt. 4. Can help consumers build their credit history. Cons: 1. Late payments may result in fees and interest charges. 2. May encourage overspending. 3. Can lead to debt problems if not managed carefully.

Features: 1. Split purchases into equal installments, typically four, with no interest or fees. 2. Shop at participating retailers online and in-store. 3. Quick and easy application process. 4. No credit check required. 5. Flexible repayment options. Pros: 1. Convenient way to spread out the cost of purchases. 2. Can help consumers budget their money more effectively. 3. May help consumers avoid high-interest debt. 4. Can help consumers build their credit history. Cons: 1. Late payments may result in fees and interest charges. 2. May encourage overspending. 3. Can lead to debt problems if not managed carefully.14. Four

Four is a Buy Now, Pay Later (BNPL) provider that allows customers to split their purchases into equal installments, typically four, with no interest or fees. It is currently available in the United States and Canada. Features: 1. Split purchases into equal installments, typically four, with no interest or fees. 2. Shop at participating retailers online and in-store. 3. Quick and easy application process. 4. No credit check required. 5. Flexible repayment options. Pros: 1. Convenient way to spread out the cost of purchases. 2. Can help consumers budget their money more effectively. 3. May help consumers avoid high-interest debt. 4. Can help consumers build their credit history. Cons: 1. Late payments may result in fees and interest charges. 2. May encourage overspending. 3. Can lead to debt problems if not managed carefully.

Features: 1. Split purchases into equal installments, typically four, with no interest or fees. 2. Shop at participating retailers online and in-store. 3. Quick and easy application process. 4. No credit check required. 5. Flexible repayment options. Pros: 1. Convenient way to spread out the cost of purchases. 2. Can help consumers budget their money more effectively. 3. May help consumers avoid high-interest debt. 4. Can help consumers build their credit history. Cons: 1. Late payments may result in fees and interest charges. 2. May encourage overspending. 3. Can lead to debt problems if not managed carefully.15. Tabby

Tabby is a Buy Now Pay Later (BNPL) service designed to make shopping more convenient and budget-friendly. Operating primarily in the United Arab Emirates (UAE) and Saudi Arabia, Tabby offers users the flexibility to make online and in-store purchases and pay for them in interest-free installments. Tabby primarily serves customers in the United Arab Emirates (UAE) and Saudi Arabia. Features: 1. Interest-Free Payments: Tabby typically offers interest-free installment plans, allowing users to divide their purchase cost into equal payments without incurring additional interest charges. 2. Quick Approval: Tabby provides a swift approval process, enabling users to complete their transactions promptly. 3. Flexible Payment Plans: Users can customize their payment plans, selecting the number of installments and the repayment frequency that aligns with their budget. 4. Online and In-Store Use: Tabby can be used for both online and in-store purchases, offering versatility for various shopping scenarios. 5. Mobile Accessibility: Tabby may offer a mobile app that allows users to manage their accounts, track payments, and access customer support conveniently. Pros: 1. Interest-Free Payments: Most Tabby installment plans are interest-free, providing users with an affordable and budget-friendly payment option. 2. Payment Flexibility: Tabby offers users the flexibility to tailor their payment plans to match their financial situation. 3. Quick Checkout: Integration with participating retailers ensures a smooth and efficient checkout process. 4. Mobile App: A mobile app, if available, enhances accessibility, allowing users to manage their accounts and payments on the go. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of purchases. 2. Limited Geographic Coverage: Tabby’s primary focus is on the UAE and Saudi Arabia, limiting availability in other regions. 3. Credit Impact: While Tabby may not conduct traditional credit checks, missed payments may negatively affect users’ credit profiles.

Features: 1. Interest-Free Payments: Tabby typically offers interest-free installment plans, allowing users to divide their purchase cost into equal payments without incurring additional interest charges. 2. Quick Approval: Tabby provides a swift approval process, enabling users to complete their transactions promptly. 3. Flexible Payment Plans: Users can customize their payment plans, selecting the number of installments and the repayment frequency that aligns with their budget. 4. Online and In-Store Use: Tabby can be used for both online and in-store purchases, offering versatility for various shopping scenarios. 5. Mobile Accessibility: Tabby may offer a mobile app that allows users to manage their accounts, track payments, and access customer support conveniently. Pros: 1. Interest-Free Payments: Most Tabby installment plans are interest-free, providing users with an affordable and budget-friendly payment option. 2. Payment Flexibility: Tabby offers users the flexibility to tailor their payment plans to match their financial situation. 3. Quick Checkout: Integration with participating retailers ensures a smooth and efficient checkout process. 4. Mobile App: A mobile app, if available, enhances accessibility, allowing users to manage their accounts and payments on the go. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of purchases. 2. Limited Geographic Coverage: Tabby’s primary focus is on the UAE and Saudi Arabia, limiting availability in other regions. 3. Credit Impact: While Tabby may not conduct traditional credit checks, missed payments may negatively affect users’ credit profiles.16. Tamara

Tamara is a Buy Now Pay Later (BNPL) service designed to provide consumers with flexible payment options for their online and in-store purchases. Operating primarily in the Middle East and North Africa (MENA) region, Tamara allows users to split their payments into interest-free installments, making shopping more accessible and budget-friendly. Tamara primarily serves customers in the Middle East and North Africa (MENA) region. Features: 1. Interest-Free Payments: Tamara typically offers interest-free installment plans, allowing users to divide their purchase cost into equal payments without incurring additional interest charges. 2. Quick Approval: Tamara provides a swift approval process, enabling users to complete their transactions promptly. 3. Flexible Payment Plans: Users can customize their payment plans, selecting the number of installments and the repayment frequency that aligns with their budget. 4. Online and In-Store Use: Tamara can be used for both online and in-store purchases, offering versatility for various shopping scenarios. 5. Mobile Accessibility: Tamara may offer a mobile app that allows users to manage their accounts, track payments, and access customer support conveniently. Pros: 1. Interest-Free Payments: Most Tamara installment plans are interest-free, providing users with an affordable and budget-friendly payment option. 2. Payment Flexibility: Tamara offers users the flexibility to tailor their payment plans to match their financial situation. 3. Quick Checkout: Integration with participating retailers ensures a smooth and efficient checkout process. 4. Mobile App: A mobile app, if available, enhances accessibility, allowing users to manage their accounts and payments on the go. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of purchases. 2. Limited Geographic Coverage: Tamara’s primary focus is on the MENA region, limiting availability in other regions. 3. Credit Impact: While Tamara may not conduct traditional credit checks, missed payments may negatively affect users’ credit profiles.

Features: 1. Interest-Free Payments: Tamara typically offers interest-free installment plans, allowing users to divide their purchase cost into equal payments without incurring additional interest charges. 2. Quick Approval: Tamara provides a swift approval process, enabling users to complete their transactions promptly. 3. Flexible Payment Plans: Users can customize their payment plans, selecting the number of installments and the repayment frequency that aligns with their budget. 4. Online and In-Store Use: Tamara can be used for both online and in-store purchases, offering versatility for various shopping scenarios. 5. Mobile Accessibility: Tamara may offer a mobile app that allows users to manage their accounts, track payments, and access customer support conveniently. Pros: 1. Interest-Free Payments: Most Tamara installment plans are interest-free, providing users with an affordable and budget-friendly payment option. 2. Payment Flexibility: Tamara offers users the flexibility to tailor their payment plans to match their financial situation. 3. Quick Checkout: Integration with participating retailers ensures a smooth and efficient checkout process. 4. Mobile App: A mobile app, if available, enhances accessibility, allowing users to manage their accounts and payments on the go. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of purchases. 2. Limited Geographic Coverage: Tamara’s primary focus is on the MENA region, limiting availability in other regions. 3. Credit Impact: While Tamara may not conduct traditional credit checks, missed payments may negatively affect users’ credit profiles.17. Opy (Formerly Openpay)

Opy is a Buy Now, Pay Later (BNPL) provider that allows customers to split their purchases into equal installments, typically four, with no interest or fees. It is currently available in the United States and Mexico. Features: 1. Split purchases into equal installments, typically four, with no interest or fees. 2. Shop at participating retailers online and in-store. 3. Quick and easy application process. 4. No credit check required. 5. Flexible repayment options. Pros: 1. Convenient way to spread out the cost of purchases. 2. Can help consumers budget their money more effectively. 3. May help consumers avoid high-interest debt. 4. Can help consumers build their credit history. Cons: 1. Late payments may result in fees and interest charges. 2. May encourage overspending. 3. Can lead to debt problems if not managed carefully.

Features: 1. Split purchases into equal installments, typically four, with no interest or fees. 2. Shop at participating retailers online and in-store. 3. Quick and easy application process. 4. No credit check required. 5. Flexible repayment options. Pros: 1. Convenient way to spread out the cost of purchases. 2. Can help consumers budget their money more effectively. 3. May help consumers avoid high-interest debt. 4. Can help consumers build their credit history. Cons: 1. Late payments may result in fees and interest charges. 2. May encourage overspending. 3. Can lead to debt problems if not managed carefully.18. LeaseVille

LeaseVille is a Buy Now Pay Later (BNPL) service that specializes in lease-to-own financing options for consumers. This service allows users to access a wide range of products, including electronics, appliances, furniture, and more, with the flexibility to make affordable lease payments over time. LeaseVille primarily serves customers in the United States. Features: 1. Lease-to-Own Model: LeaseVille offers a lease-to-own financing model, allowing users to make payments toward the ownership of the products they choose. 2. Wide Product Selection: LeaseVille provides access to a diverse selection of products, making it suitable for various consumer needs. 3. Flexible Payment Plans: Users can customize their payment plans, selecting the repayment terms and frequencies that align with their budget. 4. Online Shopping: LeaseVille typically operates online, enabling users to shop for products and complete lease agreements conveniently. Pros: 1. Product Accessibility: LeaseVille’s lease-to-own model makes it possible for users to access products they might not be able to afford upfront. 2. Flexible Payments: Users can choose payment terms that fit their financial situation, offering flexibility and affordability. 3. Wide Product Range: LeaseVille offers a broad range of products, catering to various consumer preferences and needs. 4. No Credit Checks: LeaseVille may not require traditional credit checks, making it accessible to users with varying credit histories. Cons: 1. Total Cost: Lease-to-own agreements may result in users paying more for a product compared to purchasing it outright. 2. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of ownership. 3. Limited Geographic Coverage: LeaseVille’s primary focus is on the United States, limiting availability in other regions.

Features: 1. Lease-to-Own Model: LeaseVille offers a lease-to-own financing model, allowing users to make payments toward the ownership of the products they choose. 2. Wide Product Selection: LeaseVille provides access to a diverse selection of products, making it suitable for various consumer needs. 3. Flexible Payment Plans: Users can customize their payment plans, selecting the repayment terms and frequencies that align with their budget. 4. Online Shopping: LeaseVille typically operates online, enabling users to shop for products and complete lease agreements conveniently. Pros: 1. Product Accessibility: LeaseVille’s lease-to-own model makes it possible for users to access products they might not be able to afford upfront. 2. Flexible Payments: Users can choose payment terms that fit their financial situation, offering flexibility and affordability. 3. Wide Product Range: LeaseVille offers a broad range of products, catering to various consumer preferences and needs. 4. No Credit Checks: LeaseVille may not require traditional credit checks, making it accessible to users with varying credit histories. Cons: 1. Total Cost: Lease-to-own agreements may result in users paying more for a product compared to purchasing it outright. 2. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of ownership. 3. Limited Geographic Coverage: LeaseVille’s primary focus is on the United States, limiting availability in other regions.19. FlexShopper

FlexShopper is a Buy Now Pay Later (BNPL) service that specializes in lease-to-own financing options for consumers. This service allows users to lease a wide range of products, including electronics, furniture, appliances, and more, with the option to make affordable payments over time. FlexShopper focuses on providing accessibility to products through flexible financing. FlexShopper primarily serves customers in the United States. Features: 1. Lease-to-Own Model: FlexShopper offers a lease-to-own financing model, allowing users to make payments toward the ownership of the products they select. 2. Wide Product Selection: FlexShopper provides access to a diverse selection of products, making it suitable for various consumer needs. 3. Flexible Payment Plans: Users can customize their payment plans, selecting the repayment terms and frequencies that align with their budget. 4. Online Shopping: FlexShopper typically operates online, enabling users to browse products, complete lease agreements, and make payments conveniently. Pros: 1. Product Accessibility: FlexShopper’s lease-to-own model makes it possible for users to access products they might not be able to afford upfront. 2. Flexible Payments: Users can choose payment terms that fit their financial situation, offering flexibility and affordability. 3. Wide Product Range: FlexShopper offers a broad range of products, catering to various consumer preferences and needs. 4. No Credit Checks: FlexShopper may not require traditional credit checks, making it accessible to users with varying credit histories. Cons: 1. Total Cost: Lease-to-own agreements may result in users paying more for a product compared to purchasing it outright. 2. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of ownership. 3. Limited Geographic Coverage: FlexShopper’s primary focus is on the United States, limiting availability in other regions.

Features: 1. Lease-to-Own Model: FlexShopper offers a lease-to-own financing model, allowing users to make payments toward the ownership of the products they select. 2. Wide Product Selection: FlexShopper provides access to a diverse selection of products, making it suitable for various consumer needs. 3. Flexible Payment Plans: Users can customize their payment plans, selecting the repayment terms and frequencies that align with their budget. 4. Online Shopping: FlexShopper typically operates online, enabling users to browse products, complete lease agreements, and make payments conveniently. Pros: 1. Product Accessibility: FlexShopper’s lease-to-own model makes it possible for users to access products they might not be able to afford upfront. 2. Flexible Payments: Users can choose payment terms that fit their financial situation, offering flexibility and affordability. 3. Wide Product Range: FlexShopper offers a broad range of products, catering to various consumer preferences and needs. 4. No Credit Checks: FlexShopper may not require traditional credit checks, making it accessible to users with varying credit histories. Cons: 1. Total Cost: Lease-to-own agreements may result in users paying more for a product compared to purchasing it outright. 2. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of ownership. 3. Limited Geographic Coverage: FlexShopper’s primary focus is on the United States, limiting availability in other regions.20. Perpay

Perpay is a Buy Now Pay Later (BNPL) service that focuses on providing consumers with a flexible and affordable shopping experience. This service allows users to shop for a variety of products and make payments through manageable installments. Perpay’s goal is to enhance accessibility to products while promoting responsible spending. Perpay primarily serves customers in the United States. Features: 1. Installment Payments: Perpay offers users the option to split their purchase cost into interest-free installment payments, making products more affordable. 2. Wide Product Range: Perpay provides access to a diverse selection of products, including electronics, home goods, fashion, and more. 3. Flexible Payment Plans: Users can customize their payment plans, choosing the number of installments and the repayment frequency that aligns with their budget. 4. Online Shopping: Perpay typically operates online, enabling users to browse products, complete purchases, and manage payments conveniently. Pros: 1. Affordable Shopping: Perpay’s installment payments make it possible for users to access products and pay for them over time without a large upfront expense. 2. Flexible Payments: Users can select payment terms that suit their financial situation, offering flexibility and budget-friendliness. 3. Wide Product Range: Perpay offers a broad range of products, catering to various consumer needs and preferences. 4. No Credit Checks: Perpay may not require traditional credit checks, ensuring accessibility for users with varying credit histories. Cons: 1. Total Cost: Using Perpay’s installment payments may result in users paying more for a product compared to purchasing it outright. 2. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of the purchase. 3. Limited Geographic Coverage: Perpay’s primary focus is on the United States, limiting availability in other regions.

Features: 1. Installment Payments: Perpay offers users the option to split their purchase cost into interest-free installment payments, making products more affordable. 2. Wide Product Range: Perpay provides access to a diverse selection of products, including electronics, home goods, fashion, and more. 3. Flexible Payment Plans: Users can customize their payment plans, choosing the number of installments and the repayment frequency that aligns with their budget. 4. Online Shopping: Perpay typically operates online, enabling users to browse products, complete purchases, and manage payments conveniently. Pros: 1. Affordable Shopping: Perpay’s installment payments make it possible for users to access products and pay for them over time without a large upfront expense. 2. Flexible Payments: Users can select payment terms that suit their financial situation, offering flexibility and budget-friendliness. 3. Wide Product Range: Perpay offers a broad range of products, catering to various consumer needs and preferences. 4. No Credit Checks: Perpay may not require traditional credit checks, ensuring accessibility for users with varying credit histories. Cons: 1. Total Cost: Using Perpay’s installment payments may result in users paying more for a product compared to purchasing it outright. 2. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of the purchase. 3. Limited Geographic Coverage: Perpay’s primary focus is on the United States, limiting availability in other regions.21. Postpay

Postpay is a Buy Now Pay Later (BNPL) service designed to offer consumers a flexible and convenient payment option for their online and in-store purchases. With Postpay, users can make purchases and choose to pay for them later, often in interest-free installments, enhancing their budgeting capabilities. Postpay’s geographic coverage are United Arab Emirates and Kingdom of Saudi Arabia. Features: 1. Interest-Free Payments: Postpay typically offers interest-free installment plans, allowing users to split their purchase cost into equal payments without incurring additional interest charges. 2. Quick Approval: Postpay provides a swift approval process, ensuring a seamless shopping experience. 3. Flexible Payment Plans: Users can customize their payment plans, selecting the number of installments and the repayment frequency that aligns with their budget. 4. Online and In-Store Use: Postpay can be used for both online and in-store purchases, offering versatility for various shopping scenarios. 5. Mobile Accessibility: Postpay may offer a mobile app that allows users to manage their accounts, track payments, and access customer support conveniently. Pros: 1. Interest-Free Payments: Most Postpay installment plans are interest-free, providing users with an affordable and budget-friendly payment option. 2. Payment Flexibility: Postpay offers users the flexibility to tailor their payment plans to match their financial situation. 3. Quick Checkout: Integration with participating retailers ensures a smooth and efficient checkout process. 4. Mobile App: A mobile app, if available, enhances accessibility, allowing users to manage their accounts and payments on the go. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of purchases. 2. Limited Geographic Coverage: Postpay’s availability may be limited to certain regions or countries. 3. Credit Impact: While Postpay may not conduct traditional credit checks, missed payments may negatively affect users’ credit profiles.

Features: 1. Interest-Free Payments: Postpay typically offers interest-free installment plans, allowing users to split their purchase cost into equal payments without incurring additional interest charges. 2. Quick Approval: Postpay provides a swift approval process, ensuring a seamless shopping experience. 3. Flexible Payment Plans: Users can customize their payment plans, selecting the number of installments and the repayment frequency that aligns with their budget. 4. Online and In-Store Use: Postpay can be used for both online and in-store purchases, offering versatility for various shopping scenarios. 5. Mobile Accessibility: Postpay may offer a mobile app that allows users to manage their accounts, track payments, and access customer support conveniently. Pros: 1. Interest-Free Payments: Most Postpay installment plans are interest-free, providing users with an affordable and budget-friendly payment option. 2. Payment Flexibility: Postpay offers users the flexibility to tailor their payment plans to match their financial situation. 3. Quick Checkout: Integration with participating retailers ensures a smooth and efficient checkout process. 4. Mobile App: A mobile app, if available, enhances accessibility, allowing users to manage their accounts and payments on the go. Cons: 1. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of purchases. 2. Limited Geographic Coverage: Postpay’s availability may be limited to certain regions or countries. 3. Credit Impact: While Postpay may not conduct traditional credit checks, missed payments may negatively affect users’ credit profiles.22. Zebit

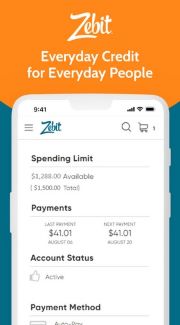

Zebit is a Buy Now Pay Later (BNPL) service that focuses on providing consumers with accessible and affordable shopping options. It offers users the ability to shop for various products and pay for them over time, often with the option of interest-free installment plans. Zebit is dedicated to helping users make responsible financial choices. Zebit primarily served customers in the United States. Features: 1. Interest-Free Payments: Zebit typically offers interest-free installment plans, allowing users to divide their purchase cost into equal payments without additional interest charges. 2. Quick Approval: Zebit provides a swift approval process, ensuring a seamless shopping experience. 3. Flexible Payment Plans: Users can customize their payment plans, choosing the number of installments and the repayment frequency that suits their budget. 4. Online Shopping: Zebit’s services are typically accessible online, enabling users to browse products, complete purchases, and manage payments conveniently. Pros: 1. Affordable Shopping: Zebit’s installment payments make it possible for users to access products and pay for them over time without a large upfront expense. 2. Flexible Payments: Users can select payment terms that align with their financial situation, offering flexibility and budget-friendliness. 3. Wide Product Range: Zebit offers a diverse selection of products, catering to various consumer needs and preferences. 4. No Credit Checks: Zebit may not require traditional credit checks, making it accessible to users with varying credit histories. Cons: 1. Total Cost: Using Zebit’s installment payments may result in users paying more for a product compared to purchasing it outright. 2. Late Fees: Missing payments or making late payments can result in late fees, potentially increasing the overall cost of the purchase. 3. Limited Geographic Coverage: Zebit’s primary focus may be on specific regions, limiting availability in other areas.